The Silicon Valley Economy Today and Tomorrow: Insights from JLL’s Director of Research

Alexander Quinn

Director of Research (NorCal), JLL

As we close out 2019, we thought it fitting to share an overview of where our regional economy stands, according to the data. So we caught up with JLL’s Director of Research (NorCal), Alexander Quinn. In his role, Quinn analyzes a diverse set of economic indicators, with a particular eye on impacts to real estate investment. Read on for his assessment of the Silicon Valley economy and where things might be heading in 2020.

Silicon Valley’s economy is one of the strongest in the world with massive economic productivity and innovation. It is why other cities around the world have coined themselves ‘the Silicon Valley of …insert place here (e.g. China, India, Europe, etc.). Relative to the rest of the state and the nation, the area remains a high-income, low-poverty region. In 2019, the Valley generated record levels of private capital and IPO activity. However, the dichotomy of unemployment rates at an 18-year low and housing prices being the highest in the nation creates a wide income gap that makes Silicon Valley a complex place with significant barriers to entry.

This current economic expansion has been led by technology where Silicon Valley has been a stalwart while creating an economic halo experience across the entire United States. It is now the longest on record. To drive the point further, the economic indicators and yield curves show a moderately growing economy with no recession flash warnings.

Although most of the data continues to reflect economic strength, we should also pay attention to signs of slowing in jobs and population growth. Of particular importance is the reduced housing construction activity when it is needed most to accommodate our growing workforce.

THE SILICON VALLEY ECONOMY TODAY

- The per-person output from Silicon Valley outweighs every other economy in the nation of all major MSAs.

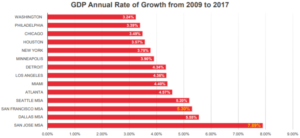

- Since the great recession, San Jose Metro Statistical Area (MSA) led the top 25 MSA in Gross Metropolitan Product. In terms of economic activity, the San Francisco/Silicon Valley mega region was the the fastest growing economy, which includes Stanford University in Palo Alto, Google’s headquarters in Mountain View, and Apple HQ in Cupertino. San Francisco MSA trails closely behind San Jose MSA, putting both areas among the top three fastest-growing MSAs in the country.

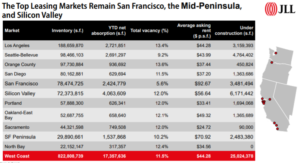

- Office vacancies are at an all-time low, with the technology industry dominating leasing activity in the Valley (Q3 2019 saw leasing activity by the tech sector of approximately 1.8M square feet!). San Francisco takes the top spot in this category with the lowest vacancy and highest asking rent, with Silicon Valley trailing close behind. In Fremont, office vacancy has decreased from 30-40% in 2010 to 5-14% in 2019.

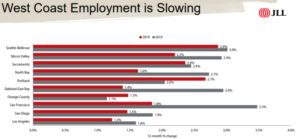

- Although the sustained demand and supply-and-demand imbalance is keeping the West Coast from correction, employment is slowing down.

STRENGTHS OF OUR ECONOMY

- The Bay Area remains the tech capital of the nation. Indicators include:

- Most active high-end innovation and software development concentration in the U.S.

- Largest cluster of higher education institutions with the top 15 colleges associated with software developer apps and social media query located in Silicon Valley.

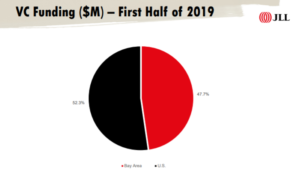

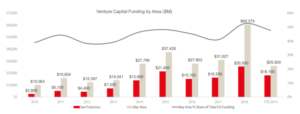

- Claims nearly half of total VC investment in the entire United States. VC funding in the Bay Area peaked in 2018 with San Francisco taking over Silicon Valley in percentage share of total funding.

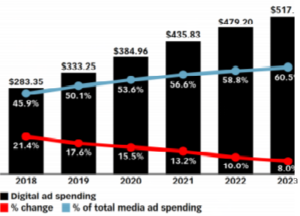

- Silicon Valley’s market share in Google and Facebook’s digital advertisement revenue accounted for more than 50% of global market share or $170 billion of the total $333 billion revenue which has been growing by double digits over the last decade. Digital ad revenue now accounts for more than half of global advertising spending and will continue to grow in market share.

LOOKING TO THE FUTURE

- Tech tenants in the market will continue to drive the demand for office space in Silicon Valley — which accounts for 61% of all requirements by product type.

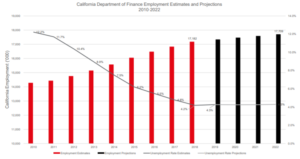

- California Department of Finance estimates indicate job growth and unemployment rate curves continuing to plateau. California EDD projects show the highest percentage share of growth in educational services (private), healthcare, and social assistance jobs.

- Migration trends indicate net loss in domestic and gains in international net migration figures since 2016. Overall, the Bay Area population growth is declining; however, the East Bay has shown an uptick in population growth since 2018.

- Housing construction continues to remain well below employment growth, creating challenges.

CLOSING THOUGHTS

While no one has a crystal ball, we all know that growth at the present rate cannot be sustained forever.

To elaborate, the major challenges that the region is facing — with more than its fair share of recent wildfires, compounded by homelessness and housing problems — act as headwinds for the economy. What makes matters worse is the fact that California has the highest individual income tax rate in the nation, an extremely high cost of living, diminishing industrial supply, rising construction costs, and other market uncertainties, leaving the region vulnerable to talent poaching from more affordable states that are activating to target Bay Area companies.

These liabilities would surely spell doom for any other place; but Silicon Valley is different. It has continued to reinvent itself, with an unmatched ability to shift from one emerging industry to the next. As with many things in Silicon Valley, it seems likely that the next downturn will serve as a natural experiment testing the strengths and vulnerabilities of the region.

We must remember the things that are integral to the region’s success — for example, the free movement of people and capital. As to how will we ride and recover should the current “gold rush” end? Only time will tell. But one thing is certain; it will be in a style typical of Silicon Valley.